The E/AI Index: Budget Architecture and the Next Phase of Enterprise AI Adoption

How CIOs and CTOs are funding AI, where deployment is moving into production, and which vendor categories are exposed as AI shifts from experimentation to budget reallocation

We have been working through the enterprise AI monetization question in the order above because the market still mistakenly compresses several different issues into one broad adoption narrative. The first report in this series focused on customer ROI and argued that AI becomes economically meaningful when it changes the cost, speed, staffing, quality, or capacity attached to a repeated unit of work. The second report moved from ROI proof to platform control and asked which layer captures the economics once those workflows move from pilot to production. This report takes the next step into budget architecture, where the AI cycle becomes easier to analyze because CIOs are now deciding which existing spend pools should fund the next wave of deployment.

An observation worth highlighting, that comes on the back of our 25+ years studying this industry, is that enterprise AI adoption will not move through the market as one uniform curve. Consumer technology has always had different adoption profiles, with early adopters, the early majority, late majority buyers, and laggards all behaving differently as a market matures. Enterprise technology follows a similar pattern, although the behaviors are shaped by budget ownership, governance, security posture, regulatory burden, data readiness, organizational complexity, and tolerance for operational risk. The most progressive enterprises are important use cases because they give us leading indicators of what may become possible. They also represent a minority of the market, and their behavior should not be treated as the steady-state adoption pattern for the long tail of enterprise buyers.

That is why we are committed to tracking the adoption path in real time rather than drawing broad conclusions from the most aggressive early adopters alone. Early enterprises can move faster, accept more deployment complexity, tolerate higher model or integration cost, and make bigger organizational changes because they often have stronger technical teams, cleaner data architecture, more executive sponsorship, or a clearer strategic mandate. The broader enterprise market behaves differently. The majority of companies move through procurement, governance, legal review, security architecture, workflow integration, and CFO scrutiny at a slower pace. That does not make the cycle less real, but it changes how we should think about timing, value capture, and the durability of current usage patterns.

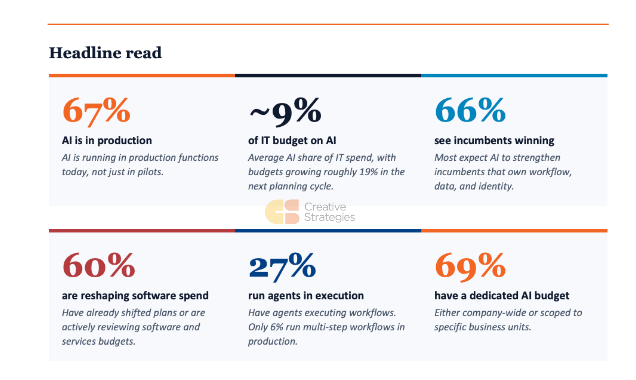

Our CIO E/AI Index work helps locate where enterprise AI sits on the adoption curve. AI has clearly moved beyond experimentation, but it remains early in terms of full-scale operating change. In the panel, 67% of respondents now have AI running in production functions, 69% have a dedicated AI budget, and AI represents roughly 9% of IT spend on average, with budgets expected to grow again in the next planning cycle. That supports the broader AI spending cycle, but the more important finding is that enterprise behavior is becoming segmented. Progressive adopters are moving faster, funding AI more deliberately, and beginning to separate what deserves scale from what stays in pilot.

The funding mix is where the budget story becomes more useful. Roughly 28 cents of the incremental AI dollar comes from net-new IT budget expansion, while the remaining 72 cents is being pulled from somewhere else inside the enterprise. Existing software budgets, IT services, systems integrators, BPO contracts, headcount savings or slower hiring, license consolidation, cloud expansion, and business-unit budgets all show up in the mix. We call this out because a dollar added to the IT envelope behaves differently from a dollar taken out of a software renewal or services contract. Enterprise AI increasingly contains both at the same time, which is why the vendor read-through is becoming more selective than the aggregate spending numbers imply.

This is also where the pricing question gets more complicated. CIOs are asking which tools can be funded from an existing cost pool, which workflows have enough measurement discipline to justify the spend, and which vendors are charging an AI premium without changing the underlying job being done. A vendor with AI attached to a governed workflow, tied to a measurable operating metric and funded from services avoidance, license consolidation, or cycle-time compression, has a stronger pricing claim than a vendor adding AI on top of a seat count the customer is already trying to rationalize.

The early ROI evidence still points toward throughput before broad labor replacement. Respondents report higher output with the same headcount, faster project delivery, lower external services spend, and slower hiring before large-scale headcount reduction. That means the first financial evidence of AI is more likely to show up in services-line compression, faster internal project cycles, reduced outside implementation capacity, slower backfill behavior, and lower unit cost inside support, development, analytics, and IT operations. Headcount reduction may come later in some categories, but it is not the first or cleanest marker of value.

The incumbent read is therefore conditional on workflow depth. Cloud infrastructure, cybersecurity, data platforms, and productivity suites screen positively because they own interfaces and control points AI must traverse to be useful and governable. Categories tied more closely to seat access, content production, manual routing, summarization, or labor-heavy services carry more risk because AI can compress the work without requiring replacement of the system of record. The full report works through that category split in detail, because the market can treat both as “software,” while CIO budget behavior is already separating the two.

Agentic AI fits the same logic. The priority is clear, but production deployment remains concentrated in bounded workflows where approval paths, data access, and auditability can be controlled. The constraints are increasingly operational: data readiness, integration, identity, permissioning, auditability, security, exception handling, and cost predictability. That suggests the next layer of enterprise AI spend should accrue not only to model access or generic copilots, but to the control plane that makes AI deployable at scale.

The practical implication is that enterprise AI should now be analyzed through budget formation and adoption-profile behavior, not adoption alone. The evidence increasingly says AI is economically meaningful, but the value will not distribute evenly across the stack or arrive uniformly across enterprise cohorts. The next phase of diligence is identifying which budget lines AI is consuming, which workflows are producing measurable returns, and which vendors can convert those returns into pricing power without triggering procurement pushback. That is where AI moves from usage to earnings power.

The E/AI Index is Creative Strategies’ recurring CIO/CTO research series tracking how enterprise AI moves through adoption profiles, budget formation, deployment maturity, workflow ROI, and vendor selection.

What paid subscribers get in the full report

The full E/AI Index dataset and adoption-profile read, including how progressive early adopters differ from the broader enterprise market and why the long tail of CIO behavior matters for sizing where we are in the AI cycle.

A budget-source model for the incremental AI dollar, separating net-new IT budget expansion from dollars being reallocated out of software, services, BPO, headcount, license consolidation, cloud, and business-unit budgets.

A category-level spend-intent map across the enterprise stack, showing where CIOs expect to increase spend, where budgets are being reviewed, and which categories screen as most exposed to AI-driven substitution.

A framework for separating real AI ROI from usage theater, focused on workflows with measurable baselines, budget owners, governance requirements, and operating denominators that procurement can actually defend.

Our read on why services compression comes before broad application replacement, including the specific kinds of SI, managed-services, implementation, testing, documentation, and support work most exposed to AI-enabled internal teams.

An incumbent-risk model based on workflow depth, distinguishing platforms with identity, data context, governance, and execution control from vendors more exposed to seat access, manual routing, content production, or shallow workflow attachment.

Updated agentic AI deployment data, including the gap between pilots, employee-assist workflows, narrow execution under human approval, and true multi-step production agents across systems.

A control-plane spending map, covering the data readiness, identity, security, auditability, observability, workflow integration, and cost-predictability layers that CIOs say are now gating broader deployment.

A risk hierarchy for enterprise AI adoption, including where CIOs are most concerned about data leakage, reliability, regulatory exposure, shadow AI, proprietary workflow exposure, and model-cost unpredictability.

The full read-through for 2026 and 2027, including what we are watching, what would change our view, and which signals would indicate AI is moving from controlled production into broader budget reallocation across the enterprise.