Qualcomm's Second Platform Moment

Data center changes the category, and custom Arm CPU may be the early upside

Although The Diligence Stack is still new as a public research product, Qualcomm is not new coverage for us. Creative Strategies has followed the company for roughly 26 years, and we have long believed the data center opportunity represented the next logical extension of Qualcomm's engineering capabilities. Two pieces of history are worth remembering before getting into this report. First, Qualcomm's 2017 Centriq Arm server CPU was widely regarded by many industry contacts we spoke with as technically strong, arriving before the Arm server ecosystem was commercially ready. Today, that environment has been fundamentally validated by hyperscalers. Second, Broadcom's 2017-2018 hostile takeover attempt reinforced our view that Qualcomm's engineering talent, IP portfolio, and technical capabilities were more valuable than the market was giving them credit for.

We attended Qualcomm's Investor Day, spent time with management, and participated in the Q&A with Akash Palkhiwala, Cristiano Amon, and Tony Pialis. We came away believing the data center opportunity is now considerably more tangible than many previously appreciated. Positioning wise, we still view Qualcomm first as a semiconductor engineering company, but data center has become the next platform leg of that engineering story.

Qualcomm used Investor Day to put a different revenue curve in front of investors. The company had already been moving beyond handsets through automotive, IoT, PC, XR, and edge AI, but that version of the story, on the surface, still looked like offset work. Automotive and IoT could help absorb Apple modem loss, Samsung mix pressure, memory-driven Android weakness, and periodic QTL renewal concern. That improved the quality of the business, but it did not force investors to place Qualcomm in a different category.

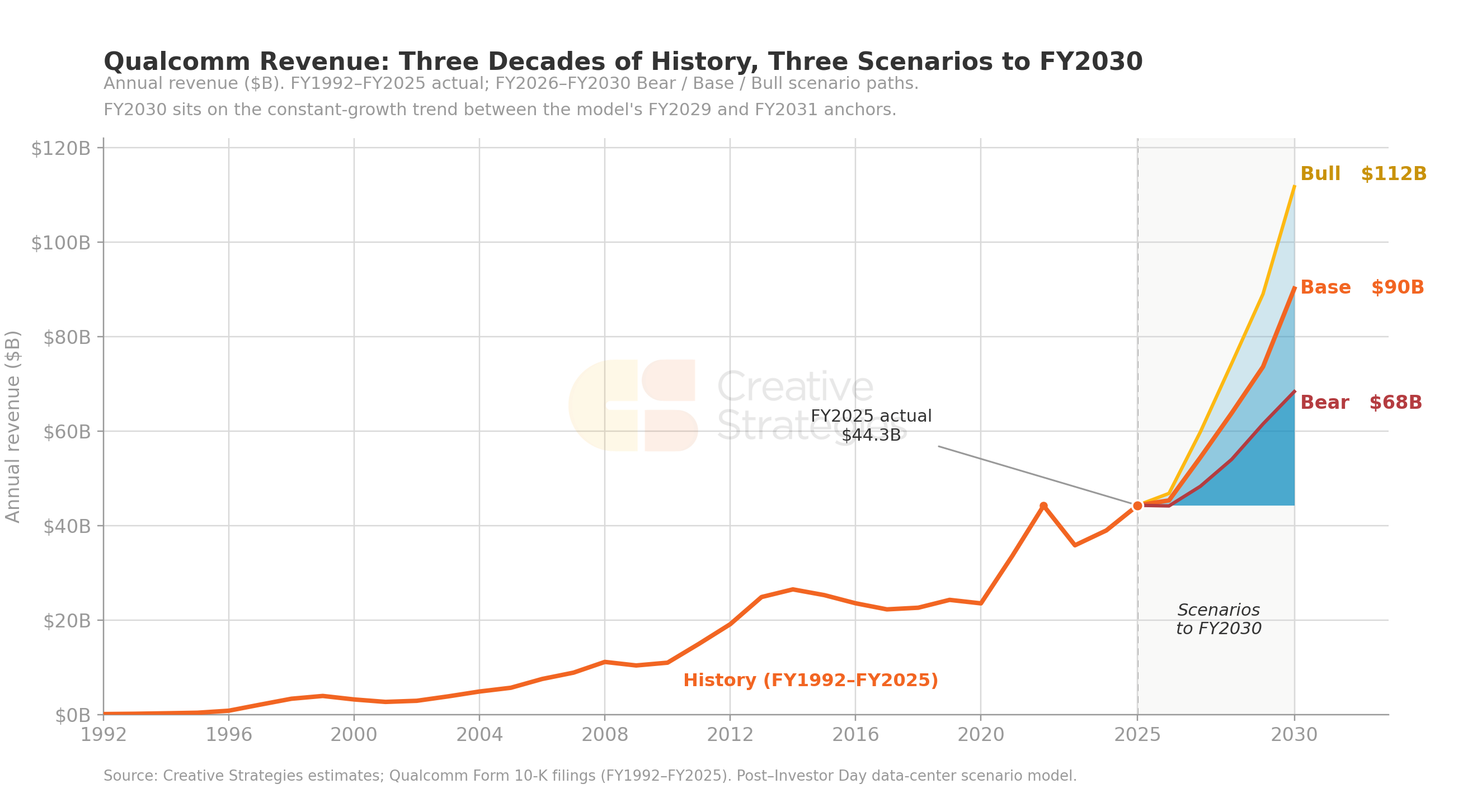

Chart for visual effect. We detail our entire model and assumptions for each revenue case in the full report and our estimate scenarios carry out to 2030.

As the chart above visualizes, the data center framework changes Qualcomm’s growth trajectory. Management raised its FY29 non-handset QCT target to $40B, roughly twice the prior FY29 target, and put a more than $15B FY29 data center target inside that number. CFO Akash Palkhiwala also made the mix change direct: by FY29, handsets are expected to fall toward roughly one-third of QCT revenue. That is the cleanest stat from the day on how the diversity story has evolved with data center now in the picture. Qualcomm can still be one of the most important mobile silicon companies in the world, while the investment argument increasingly depends on whether it becomes an edge-to-data-center AI compute platform.

We came away from the event and follow-up Q&A believing the data center narrative is more concrete than many investors assumed going in. The FY27 anchor is custom silicon-led, with two global hyperscale customers each contributing at least $1B according to management’s Q&A comments and both with multi-generational programs planned. The product cadence then layers in HBC-based AI acceleration and C1000 server CPUs. This sequence reduces the burden on any one product line. Custom silicon creates the first revenue line, CPU creates the more lasting hold on the socket, HBC gives Qualcomm an inference architecture of its own, and Alphawave adds the I/O, die-to-die, SerDes, optical, and chiplet assets that make the platform story more credible.

The custom Arm CPU point deserves more attention than it has received. Agentic AI increases host-side work inside the data center. Tool calls, retrieval, API routing, state management, security, scheduling, and accelerator coordination all run through the CPU complex. If hyperscalers want a standard Arm server CPU path, Arm CSS is available. If they want a more specialized Arm CPU with custom cores, chiplets, high-speed I/O, memory attach, and implementation help, the external partner list narrows quickly. Qualcomm’s Oryon work, architecture-license position, mobile-to-auto CPU experience, and Alphawave connectivity assets give it a credible claim to that role.

HBC is the second technical piece to understand. High Bandwidth Compute is Qualcomm’s answer to the inference memory bottleneck. Traditional accelerator systems spend power and packaging budget moving data between compute and external memory stacks. Qualcomm’s approach places the XPU under DRAM stacks so the compute sits closer to memory. The claim is SRAM-like performance with DRAM-class density, with better bandwidth per watt and capacity per watt across different inference workloads. The business read-through is cost per token, rather than a generic accelerator benchmark. We view this as interesting, needing further proof, but we know much of the industry has been circling around how to do near memory compute, mostly in RND, so this could be validation for that approach which will also make LPDDR a strategic part of compute packaging.

Our scenario model frames the change. The bear case takes Qualcomm to roughly $61.5B of FY29 revenue with $10B from data center. The base case, which largely follows management’s Investor Day framework, reaches roughly $73.6B of FY29 revenue with $15B from data center. The bull case reaches roughly $89B of FY29 revenue with $22B from data center, driven mainly by custom Arm CPU absorption and HBC/connectivity attach above the initial guide. In the base case, Qualcomm grows well beyond the pre-event low/mid-$40B revenue framing. In the bull case, the business is roughly twice its FY25 revenue base by FY29.

That is the reason we frame this as Qualcomm’s second platform moment. The first platform was mobile. The second is the attempt to extend Qualcomm’s compute, connectivity, and low-power design DNA into data center AI infrastructure while keeping the edge portfolio compounding. Data center is the growth driver. Automotive, industrial, robotics, personal AI, PC, XR, and QTL make the bridge less fragile. The diligence question is now whether $15B is a ceiling, or the first visible layer of a larger custom silicon platform business.

Inside the full subscriber report

The pre- and post-Investor Day revenue bridge: why the old model looked like offset work and the new model changes the category.

A full scenario model through FY31, including bear/base/bull revenue paths and the EV/sales read-through at each path.

A data center stack that separates custom Arm CPU, custom ASIC services, HBC acceleration, and Alphawave connectivity/IP.

Why custom Arm CPU may be the more lasting upside layer if hyperscalers move beyond standard Arm CSS building blocks.

An explanation of HBC and why its economic value is tied to memory movement, bandwidth per watt, and cost per token.

A full FY29 business breakdown showing how auto, industrial, robotics, personal AI, PC, XR, and QTL contribute around the data center ramp.

What would change our view. The operating variables that would make us more constructive or force us to reduce the data center multiple credit.